AA (Vic) recently hosted a Hotel Market and Economic Outlook member event. Adam Donaldson, Commonwealth Bank Head of Market Strategy and Rates Research outlined key global events and relevant macroeconomic variables that are currently shaping market conditions.

Key themes

The Middle East conflict is significantly contributing to uncertainty of supply and increased production costs of a range of materials that are critical to the efficient functioning of Australia’s economy.

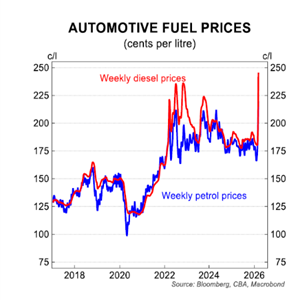

Oil supply, obviously central to the production of petrol and diesel, is volatile and prices are elevated, sitting at $US112 per barrel currently, with the potential to range between $US120-$US150 in the coming months, dependent on the conflict’s length. By contrast, the average price across 2025 was $US69. Heightened transport costs translate to higher prices for a range of goods, including fuels, plastics and computer hardware (requires helium), that has created panic buying and stockpiling by some consumers and trade customers.

Australia’s labour market is tight and unemployment remains low (circa 4.25%) as resulting wage rise pressure increases costs of production and translates to higher prices. Job growth across Australia is tracking at circa 2% annually, a good news story, in otherwise uncertain times. Previous government energy price concessions have concluded, contributing to price spikes of circa 20% between late 2025 into 2026, according to the Australian Bureau of Statistics (ABS). The initial catalyst for these price spikes was the conflict between Russia and the Ukraine, when Russian energy supply was cut (previously supplied 35%-40% of Europe’s natural gas). Commonwealth Bank of Australia (CBA) expects price pressure to continue across the Australian winter, with the Federal Government’s ability to provide further rebate relief to consumers limited given our current inflation scenario.

Inflationary pressures spark interest rate movements

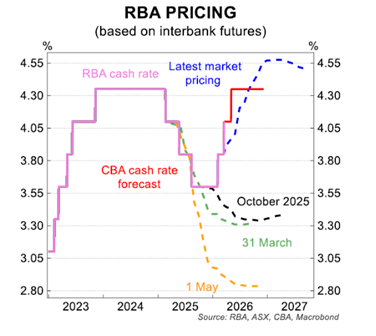

The ABS reported Australia’s inflation rate in the year to December 2025 was 3.8%, trending above the Reserve Bank of Australia (RBA) target (between 2%-3%). Interest rate rises are designed to reduce prevailing inflationary pressures, by reducing consumption and related product/service demand. CBA note “a significant change in Australia’s interest rate story of +1.7% since May 2025, with two recent interest rate rises, just six months post the RBA’s last rate cut.” On the balance of probabilities, CBA expect another 0.25 basis point cash rate rise in May 2026. Cash rate movements coincide with a “radical rethink on Australia’s inflation projections by the RBA,” that could get as high as 4.5%-5% over the next 18 months, without their intervention.

Inflationary pressures spark interest rate movements

The ABS reported Australia’s inflation rate in the year to December 2025 was 3.8%, trending above the Reserve Bank of Australia (RBA) target (between 2%-3%). Interest rate rises are designed to reduce prevailing inflationary pressures, by reducing consumption and related product/service demand. CBA note “a significant change in Australia’s interest rate story of +1.7% since May 2025, with two recent interest rate rises, just six months post the RBA’s last rate cut.” On the balance of probabilities, CBA expect another 0.25 basis point cash rate rise in May 2026. Cash rate movements coincide with a “radical rethink on Australia’s inflation projections by the RBA,” that could get as high as 4.5%-5% over the next 18 months, without their intervention.

The causes of inflation are increasingly complex as a demand and supply imbalance is evident across Australia’s economy. This creates product/service shortages and operational inefficiencies (e.g. higher costs of production and inventory control challenges). Productivity measures are a priority for the Federal Government, given the production of more goods/services more efficiently is a significant generator of economic growth. An acceleration in household demand, across Jul-Dec 2025, was “significantly stronger” than the RBA had expected. Gross Domestic Product, measuring the total value of goods and services produced in Australia’s economy rose by 2.6% across the 2025 calendar year.

Our economy’s potential growth rate measures its sustainable growth without stimulating excessive inflation. At +2.6%, GDP growth currently exceeds the RBA’s view of ideal economic output growth (circa 2% annually) and could be a catalyst for the RBA Board to consider future cash rate rises. CBA note “huge volatility in real household incomes across the past eight years” given, the impact of the COVID pandemic, increased consumer taxes and borrowing costs.

18 months, without their intervention.

Increased spending fueling inflation

CBA note these factors negatively impact consumer spending, which they expect to moderate, post the recent 2025 uptick. There has been a noticeable increase in private sector business investment, particularly driven by the Artificial Intelligence (AI) boom and a significant uptick in data centre construction spend, the scale of which was unexpected.

The Centre for Independent Studies note substantial spending on infrastructure projects and the care economy, particularly aged care and National Disability Insurance Scheme-related, has inflated government spending in recent years. Adding, “the community’s expectations of government have outgrown its economic capacity to respond responsibly, and only government itself can reset those expectations.”

CBA agree government needs to do its part to slow down spending, so as to not add to inflationary pressures already evident across our economy. This following a sustained “10-year capital expenditure boom” across Australia, fuelled in recent years by defence and AI-related spending.

Rising rents and house prices add to an already uncomfortable inflationary picture, particularly in Brisbane and Perth. These price growth trends are more muted in Melbourne and Sydney. CBA reflecting that interest rate rises are somewhat of a harsh reality for consumers, following a 30-year period from the 1990’s through to the COVID pandemic where they fell, on a trend basis. During this period, the RBA describe the creation of a “global savings glut,” where low interest rates contributed to global savings significantly exceeding global capital investment. CBA contend that interest rate rises are not an anomaly, predicting they are unlikely to return to these levels.

Implications for accommodation hotels

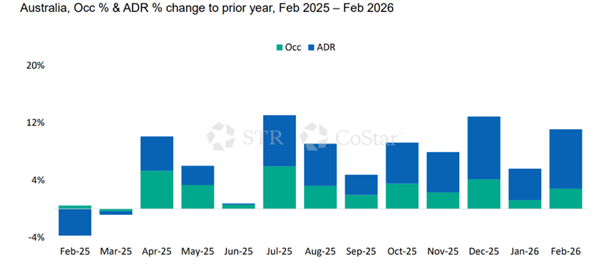

CoStar (formerly STR) report global accommodation demand is trending positively (YoY), with Asia-Pacific “the engine room” of this post-pandemic growth. Australia possesses strong demand driving fundamentals, that compare well to many Asian countries.

Source: CoStar

CoStar note that movements in travel demand relating to the Middle East conflict are much sharper than were experienced during COVID. As proven previously, travel spend is remarkably resilient, with international source markets expected to rebound quickly, once the conflict ends. In the interim, travel flows have obviously been disrupted, as travellers look to avoid transiting through the Middle East region. Increased demand, reduced flight frequencies and rising airline operating costs combining to drive airfares higher. Increasingly, Australia is seen as a safe haven for travel and investment, with a relatively stable political climate, far removed from world conflicts. These factors are expected to have a demand-positive flow on effect, once as traveller behaviour normalises. Conceivably, an uptick in domestic and Asia-Pacific Rim travel could also materialise, as Australians, not willing to risk getting stuck and face large, related costs, choose the safety and certainty of travelling at, or near, home.

fundamentals, that compare well to many Asian countries.