In recent years, surcharging has become a hot topic among pubs in Australia. With tight regulations and increased consumer awareness, it is crucial for pub owners to understand and comply with surcharge laws to avoid penalties and maintain customer trust. This guide aims to provide pubs in Australia with the necessary information to navigate surcharge laws effectively.

Understanding Surcharge Regulations:

Surcharging involves charging customers an additional fee for using certain payment methods, like credit or debit cards.

- In Australia, the Competition and Consumer Act 2010 and the Payment Systems Regulations 2016 regulate surcharges, ensuring they reflect the actual cost of processing the payment.

- Excessive surcharges are illegal, and the Australian Competition and Consumer Commission (ACCC) is scrutinising the hospitality sector closely.

- Venues can only charge what it costs them.

As you’d likely know it’s common and legal for businesses to add a surcharge to card transactions. However, with different card types and varying surcharges, publicans need to be cautious about adhering to the regulations.

The ACCC is currently taking a closer look at the hospitality segment, imposing substantial fines on businesses for excessive surcharging. Venues found guilty of these violations not only face financial penalties but also suffer severe reputational damage.

The ACCC is actively enforcing compliance by issuing ‘Surcharge Information Notices’ and fining businesses that are profiting from surcharging. These notices require businesses to provide documentation like their merchant statements, which state the merchant’s Cost of Acceptance.

If your venue isn’t following the latest surcharging laws, you could be next. The penalties for non-compliance can be severe.

- Issue of infringement notices with penalties up to $12,600 for a body corporate or $126,000 for a listed corporation.

- Court action seeking penalties up to $1,358,910 per contravention, along with injunctions and other orders.

ACCC Deputy Chair Mick Keogh pulls no punches when discussing surcharging and their view on it.

“This decision is a warning to businesses that choose to impose surcharges. The onus is on them to get it right. A failure to comply with these laws may result in significant penalties.”

Excessive Surcharging: Know the Limits

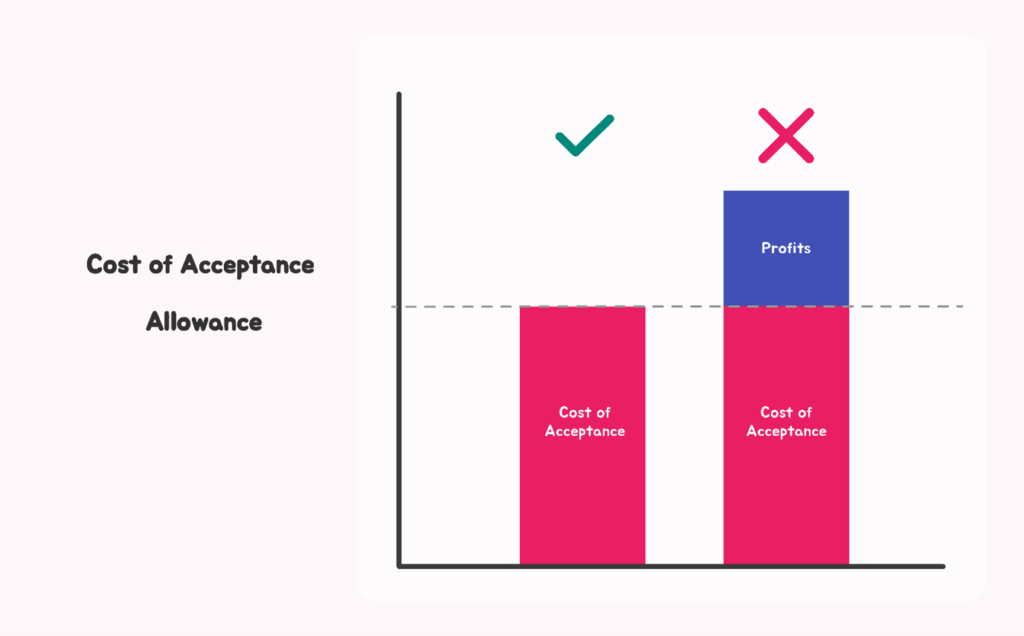

The law ensures surcharges don’t exceed the actual Cost of Acceptance. Your Cost of Acceptance is the amount it costs you to process a payment from a particular type of card. You can find your Cost of Acceptance on the statements from your Payment Service Provider or Bank. This cost is the maximum of what you can on-charge to your customer.

Rules when calculating a surcharge

The lowest surcharge: This is to be used if you want to set the same surcharge for all payment types.

For example,

- If the average Cost of Acceptance for Visa debit is 1.1% and for Visa credit it is 1.5%, and you want to charge a uniform surcharge, it must be 1.1%, the lower rate. Averaging these costs is not permitted.

- If you are on a blended rate of 1.5% for all card types, you can surcharge the full 1.5% for all transactions, whilst being fully compliant.

Flat Fee: Can be used rather than a percentage surcharge, but it must not exceed your cost for that payment type. This method should not be applied to small transactions where the fee would be disproportionate to the purchase amount.

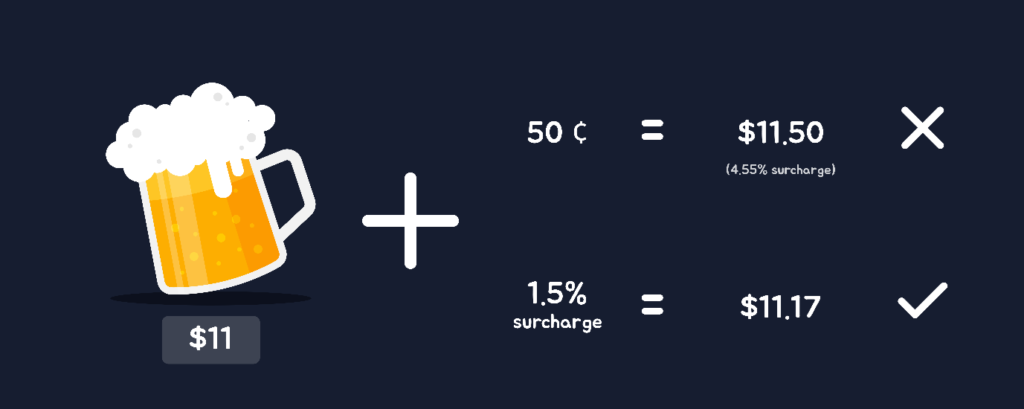

For example, for a meal of $50.00 at the pub, a 1.5% surcharge would make the total $50.75. Or for a pint of beer that costs $11.00, the surcharge at 1.5% would be $0.17. So, you can charge the customer up to $11.17.

If you charge a fixed surcharge, like $0.50 per transaction, which is $11 in this case, then you would be overcharging the customer at a 4.55% card surcharge.

No way for a consumer to pay without paying a surcharge:

If you don’t accept cash and surcharge all card payments, you must include the minimum surcharge in the displayed price of your products.

For more information around this please visit the ACCC.

Blended Rate vs. Varying Card Fee

Managing card fees can be complex due to the different rates associated with various card types, such as Visa, MasterCard, American Express, International and Corporate Cards.

Charging a flat rate of x cents per transaction can be challenging as it may lead to overcharging customers. While you can set the rate at the minimum card fee to avoid overcharging, this often results in losses when processing international and corporate cards.

To comply with regulations and avoid excess surcharges without making a loss, businesses have two main options:

Display Different Surcharges: Clearly display the different surcharge for each card type.

Blended Rate: Meaning one fixed card surcharge for all card types. Keeping it simple and transparent for your punter.

Keep your Surcharges in Check

To ensure your venue complies with ACCC rulings and avoids hefty fines and reputational damage, follow surcharge laws and avoid excessive surcharging.

Key take aways if you surcharge:

- Publicly display the correct signage indicating the surcharge percentage or amount for each applicable card.

- Surcharge your actual Cost of Acceptance. Don’t risk making an extra buck.